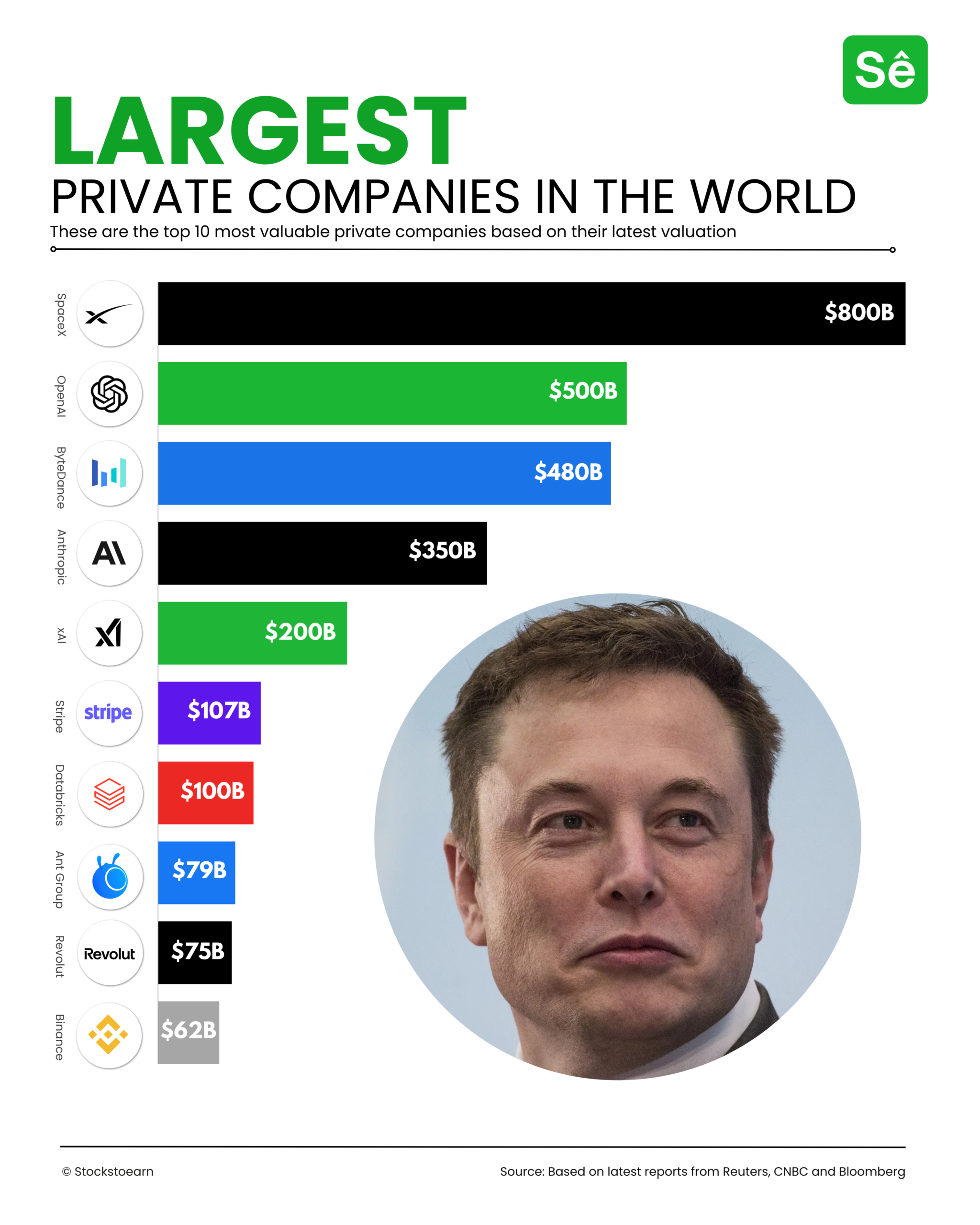

Top 10 Most Valuable Private Companies In The World Top 10 Most Valuable Private Companies In The World Read More »